For the half-year convention, you treat property as placed in service or disposed of on either the first day or the midpoint of a month. If your property has a carryover basis because you acquired it in a nontaxable transfer such as a like-kind exchange or involuntary conversion, you must generally figure depreciation for the property as if the transfer had not occurred. However, see Like-kind exchanges and involuntary conversions, earlier, in chapter 3 under How Much Can You Deduct; and Property Acquired in a Like-kind Exchange or Involuntary Conversion next. You figured this by first subtracting the first year’s depreciation ($2,144) and the casualty loss ($3,000) from the unadjusted basis of $15,000.

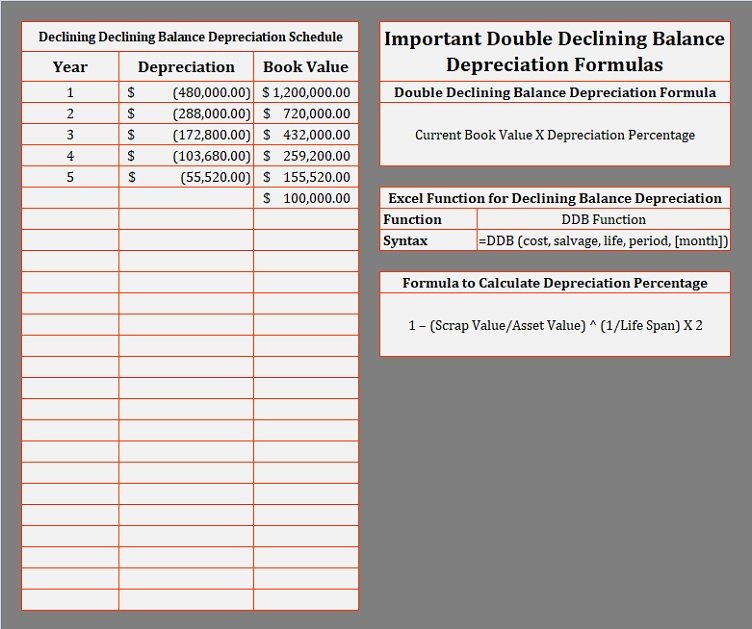

Calculating Depreciation Expense Using DDB

It loses a certain percentage of that remaining value over time because of how it’s driven, its condition, and other factors. You can connect with a licensed CPA or EA who can file your business tax returns. The DDB method is particularly relevant in industries where assets depreciate rapidly, such as technology or automotive sectors. For example, companies may use DDB for their fleet of vehicles or for high-tech manufacturing equipment, reflecting the rapid loss of value in these assets. Eric is an accounting and bookkeeping expert for Fit Small Business. He has a CPA license in the Philippines and a BS in Accountancy graduate at Silliman University.

Do you already work with a financial advisor?

There are scenarios where adjustments may be needed in DDB calculations. For instance, if an asset’s market value declines faster than anticipated, a more aggressive depreciation rate might be justified. Conversely, if the asset maintains its value better than expected, a switch to the straight-line method could be more appropriate in later years. Salvage value is the estimated resale value of an asset at the end of its useful life.

Ask a Financial Professional Any Question

The unadjusted depreciable basis and depreciation reserve of the GAA are not affected by the sale of the machine. The depreciation allowance for the GAA in 2024 is $3,200 [($10,000 − $2,000) × 40% (0.40)]. For information on the GAA treatment of property that generates foreign source income, see sections 1.168(i)-1(c)(1)(ii) and (f) of the regulations. You can use either of the following methods 5 necessary management traits of operations leaders to figure the depreciation for years after a short tax year. The following table shows the quarters of Tara Corporation’s short tax year, the midpoint of each quarter, and the date in each quarter that Tara must treat its property as placed in service. To determine the midpoint of a quarter for a short tax year of other than 4 or 8 full calendar months, complete the following steps.

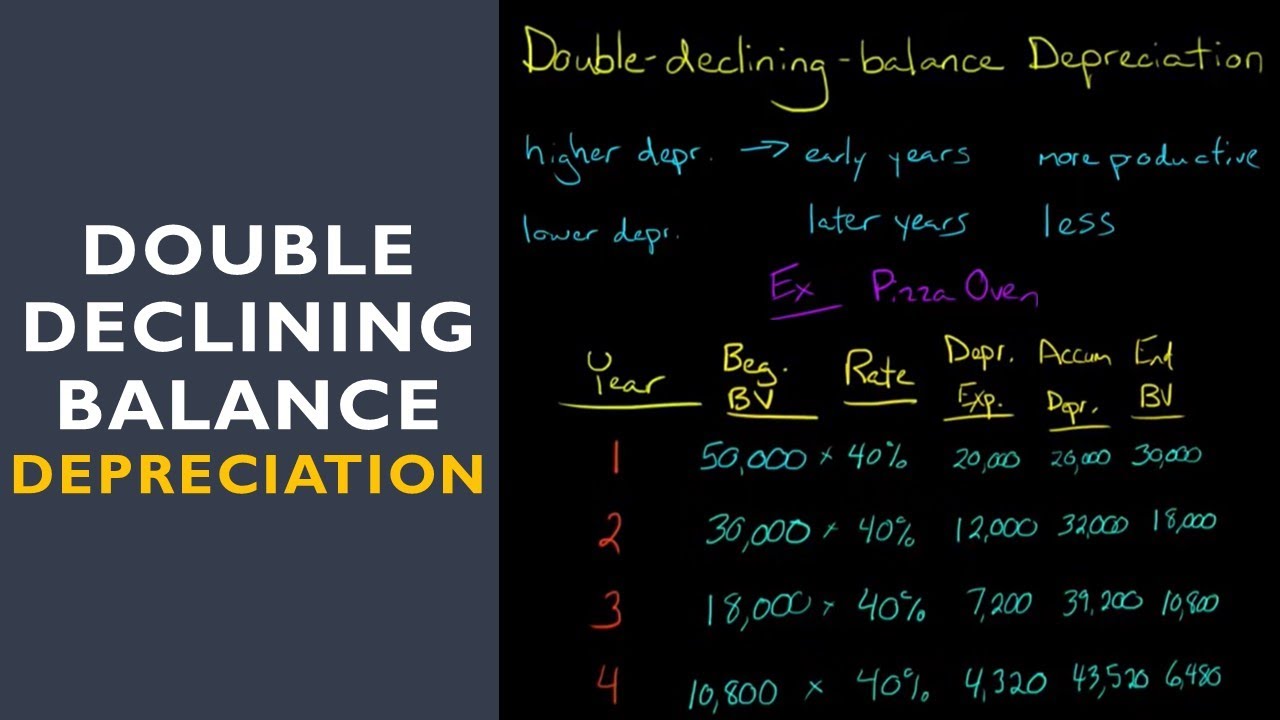

Disadvantages of the Declining Balance Method

While the straight-line depreciation method is straight-forward and most popular, there are instances in which it is not the most appropriate method. Assets are usually more productive when they are new, and their productivity declines gradually due to wear and tear and technological obsolescence. Thus, in the early years of their useful life, assets generate more revenues.

Salvage Value and Book Value: How Double Declining Balance Depreciation Method Works

As a result, the loss recognized in 2023 for each machine is $760 ($5,760 − $5,000). Under the simplified method, you figure the depreciation for a later 12-month year in the recovery period by multiplying the adjusted basis of your property at the beginning of the year by the applicable depreciation rate. Instead of using the rates in the percentage tables to figure your depreciation deduction, you can figure it yourself. Before making the computation each year, you must reduce your adjusted basis in the property by the depreciation claimed the previous year(s). If you sell or otherwise dispose of your property before the end of its recovery period, your depreciation deduction for the year of the disposition will be only part of the depreciation amount for the full year. You have disposed of your property if you have permanently withdrawn it from use in your business or income-producing activity because of its sale, exchange, retirement, abandonment, involuntary conversion, or destruction.

- On December 2, 2020, you placed in service an item of 5-year property costing $10,000.

- Your spouse has a separate business, and bought and placed in service $300,000 of qualified business equipment.

- The use of property to produce income in a nonbusiness activity (investment use) is not a qualified business use.

- For passenger automobiles and other means of transportation, allocate the property’s use on the basis of mileage.

- If the activity or the property is not included in either table, check the end of Table B-2 to find Certain Property for Which Recovery Periods Assigned.

Computer equipment for instance has better functionality in its early years. Computer equipment also becomes obsolete in a span of few years due to technological developments. Using reducing balance method to depreciate computer equipment would ensure that higher depreciation is charged in the earlier years of its operation. Similar things occur if the salvage value assumption is changed, instead. Suppose that the company changes salvage value from $10,000 to $17,000 after three years, but keeps the original 10-year lifetime. With a book value of $73,000, there is now only $56,000 left to depreciate over seven years, or $8,000 per year.

The declining balance method is a type of accelerated depreciation used to write off depreciation costs earlier in an asset’s life and to minimize tax exposure. With this method, fixed assets depreciate more so early in life rather than evenly over their entire estimated useful life. Instead of using the 150% declining balance method over a GDS recovery period for 15- or 20-year property you use in a farming business (other than real property), you can elect to depreciate it using either of the following methods. If you made this election, continue to use the same method and recovery period for that property. On July 1, 2023, you placed in service in your business qualified property (that is not long production period property or certain aircraft) that cost $450,000 and that you acquired after September 27, 2017.